A Summary of Our Newly Published Research on Target Date Funds

It is an interesting and sometimes contentious policy question how retirement wealth should be managed, especially for relatively uninvolved or uninformed investors. Governments have taken an active role in allowing certain investments for retirement plans, and disallowing others. Plans which require little intervention, but still keep retirement savings safe, are favored for less market-savvy future retirees, but some plans may be better strategies than others. Some plans deemed “safe” may even leave investors completely exposed to “black swan” events or even foreseeable losses in portfolio value.

Clearly it is necessary to invest in some risky assets in order for a portfolio to grow optimally. Should the portfolio’s risk profile be planned out entirely in advance, or follow some more adaptable plan? If the risk is planned out, is it better to spread it evenly across the savings period or to bunch it up at certain periods? A responsible manager would obviously prefer to take more risk in bull markets, and less in bear markets, but if the plan is passively managed and mapped out in advance, should an investor take more risk early (or late) in the savings period?

Target Date Funds attempt a planned shift in risk exposure to earlier in the investment phase. They have become quite popular as default retirement plans in recent years. In the US, SEC regulations allow these funds as safe harbor investments, also known as Qualified Default Investment Alternatives, protecting employers who offer these plans from fiduciary liability and providing a perhaps undeserved sense of safety to investors. The defining characteristic of these funds is the glide path, which sets a changing pattern of risk-taking over the investment period. The assumption driving these glide paths is that it is safer to assume risk early in the investment cycle. Risk is then “tapered down” so that at the time of retirement, the holdings are mostly in lower-risk assets such as treasuries or other fixed-income investments.

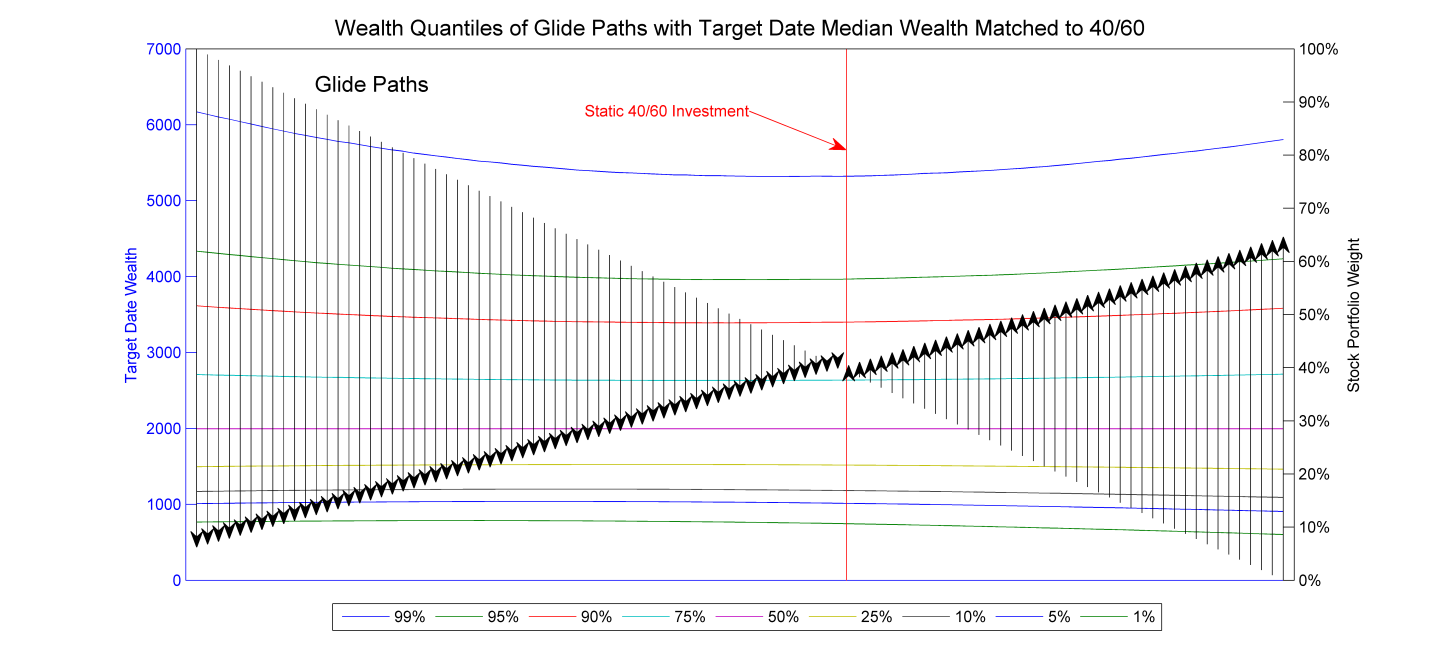

In their article, “The False Promise of Target Date Funds,” appearing in the January/February issue of the Journal of Indexes, authors David Esch and Robert Michaud of New Frontier show that glide paths add no meaningful value to the investment strategy. In the article, various glide paths are applied to a simple Monte Carlo simulation of a 40-year investment period. Many simulations are used to precisely evaluate the risk characteristics and outcomes of each path. The authors find that the uncertainty of wealth at retirement is not appreciably different for a decreasing-risk glide path than for a static balanced investment, or even a reverse glide path that increases risk as retirement nears. Indeed, many glide paths, with both deceasing and increasing risk-taking over the investment period, have exactly the same accumulated risk at retirement. In the article, families of glide paths are solved for and presented with matching risk at target date. An example of such a family appears in the graphic below. The less extreme paths in the family may also show more stable behavior under extreme market conditions, since their exposures to either asset are limited during extreme events.

The illustration here is similar to one from the article. Each black arrow stands for a glide path, with the tip of the arrow positioned at the final stock percentage of its glide path. The tail of the arrow is the starting percentage of stocks, at time 0. The stock percentages can be read from the scale on the right hand side. Thus, the arrow on the far left represents a glide path that starts at 100% stocks and ends with less than ten percent stocks, and the arrow on the right corresponds to one starting with 100% bonds and gradually increasing the stock holdings from 0% to over 60% at retirement. The red vertical line represents a static 40/60 portfolio, which has the same retirement wealth risk as all of the glide paths shown on the chart. The ranges of the simulated final wealth amounts are shown by the variously colored horizontal curves, aligned horizontally with each arrow. The wealth amounts at retirement for these curves are on the scale on the left side of the plot. Clearly, the choice of glide path itself does not have a big impact on retirement wealth, which depends far more on the behavior of the markets during the investment cycle. The full article goes on to show that the conclusions from this chart hold up under many different market assumptions and scenarios.

Given the set-in-advance rigidity of TDFs and their inability to adapt to changing market conditions or new personal circumstances, the ease with which a static investment can be adjusted to changing personal or market circumstances, and the results of this article, it is clearly preferable to invest in a balanced risk-controlled strategic portfolio. A fixed glide path leaves open the possibility to accommodate strategic changes to the portfolios to take advantage of market cycles, if the investor decides to take a more involved approach to retirement wealth management. Relatively uninformed investors are probably not comfortable with exposure to any extreme bets and are best served by a strategic portfolio somewhere in the middle of the risk spectrum. The fixed portfolio strategy is a better default alternative than a glide path, which may prove to be a bad match to markets. For example, in today’s markets, a glide path investor nearing retirement would have mostly missed out on the recent rally of the U.S. stock market because of reduced equity exposure. A fixed default portfolio such as one of New Frontier’s global strategic model portfolios leaves open the possibility of intervention to secure a better chance of a comfortable retirement, but is more likely to protect poorly informed investors who do not intervene because of its superior diversification.

Need more information?

Contact us to find out how we can work with you.