Key Takeaways

- The market is unusually disconnected from today's economy. The market is focused on the future of AI rather than the near-term economy. Most of the market’s value is a claim on a future economy.

- Markets are reacting asymmetrically. The war's end mattered to markets; its continuation did not, since it has little effect on the future success of AI.

- Index labels cannot tell the two economies apart. Growth and value indices must split the market by construction, but a market dominated by growth forces future-economy companies into value indices.

- Popular diversifiers are exposed to AI. Emerging markets, value indices, and even REITs sold as alternatives to U.S. technology hold AI components.

- Own both economies deliberately. The future economy will arrive in some form; today's economy will adapt and hold value within it. Diversified exposure to both is the answer.

Executive Summary: The Market of the Future Economy

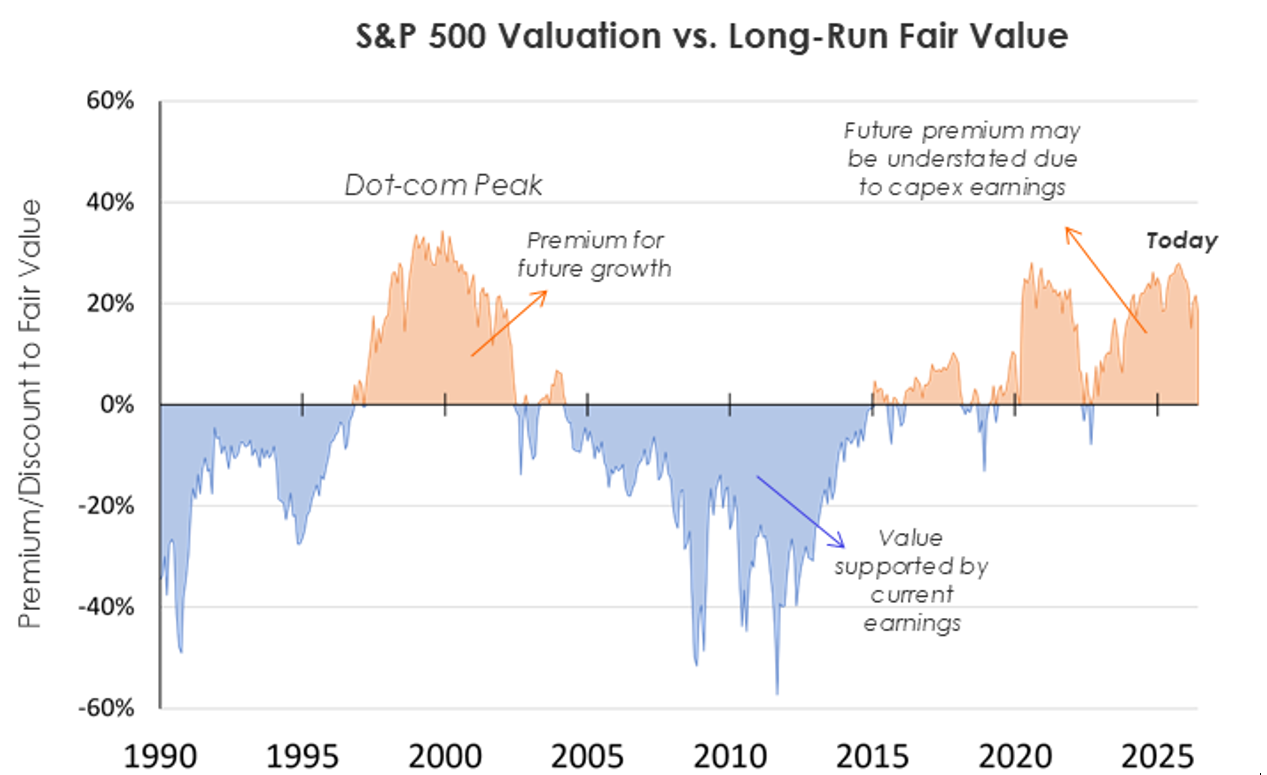

Today's market does not represent today's economy. The ratio of market value dependent on future economic activity versus present activity has never been higher. These companies have earnings now, but those earnings stem from investments in the future, not present consumption. This is the most future-weighted market in history. Even at the height of the dot-com bubble, valuations were at least aspirationally tied to virtual businesses participating in the real economy. Today, valuations are tied to an economy that does not yet exist.

The technological limits of AI are still unknown, and its ultimate success will depend on its own properties. Its pace depends on investment and informed application, but the future value of AI is little affected by even dramatic global events. It is no wonder markets ignore significant military action unless it threatens to slow the buildout of the AI future.

The question for investors is how much of their wealth to invest in this vision of the future economy and how much in today's. There is little doubt that AI will change the future, and even less that much of today's economy will adapt to that future and continue to have value in it. We want diversified exposure to both.

Economic Insights

Growth and Inflation

For all the drama in prices, the underlying economy had an unremarkable quarter. Growth remained mixed and labor markets were muted, and the war impacted inflation: May headline/core PCE remains above the Fed’s target at 4.1%/3.4%.

This plateau will likely prove sticky because inflation is asymmetric: prices rise quickly and fall slowly. For instance: Apple raised prices this quarter as memory prices surged with AI demand, but will not lower them when prices fall. Tariffs raised prices last year while the rebates from the Supreme Court's ruling became corporate profit. The future economy is taxing the present one: AI demand for chips has raised the price of phones, cars, and everything that computes. Investment in the future is showing up as inflation today.

Deglobalization and Trade

Deglobalization continued beneath the headlines. Countries keep investing in independence across energy, defense, manufacturing, and technology. These transitions reverse specialization and are inherently inflationary, while the resulting policy divergence makes international markets more valuable as diversifiers.

Trade policy has decreased in magnitude and frequency since the Supreme Court struck down the tariff regime in February. Less inflationary and less uncertain is an improvement on both counts, and markets favor it. Fiscal policy remains stimulative.

AI Capital Expenditure

The most significant economic force remains AI capital expenditure. Once again, expectations of massive investment were exceeded; AI is proving to have an insatiable appetite for computational infrastructure. The buildout is creating shortages in energy, grid, and above all chips, raising prices. The pattern is unusual: AI investment is inflationary, hard on the jobs it automates, and excellent for economic output, and all three effects are growing with the accelerated spending.

The Fed and Interest Rates

The Federal Reserve changed chairs in May. Kevin Warsh's first meeting delivered a hawkish tone: rates held at 3.5% to 3.75%, a median projection now implying a hike this year, a shorter statement, less guidance, and no dot of his own.

The new chair is less transparent by design and considers surprise a policy tool. Whether that serves an economy already high on the uncertainty scale is questionable, since uncertainty reduces activity whatever the intention. Still, early evidence is reassuring: Warsh has acted according to recognizable rules, the market response has been orderly, and the 2-year yield has drifted steadily above the funds rate, indicating investors expect a raise and that the Fed retains credibility for fighting inflation. This is good news for skeptics: Warsh intends to use the Fed's tools differently, but so far he is taking the role thoughtfully and seriously.

Market Insights

Source: Bloomberg

Asymmetric News and Momentum

The future economy led the market: chips, servers, and AI software. Today's market, the companies serving the present economy, recovered but did not lead. Markets rallied on the ceasefire and largely ignored subsequent setbacks, because the average investor dollar cares far more about building the AI future than about the current economy. The market weighs news by its effect on the future economy, and most news, including a war, affects mainly the present one.

It was a quarter for momentum: part sensible return to prior prices after a shock passed, part a fresh surge into AI trades, amplified by fortuitously timed rebalancing that reinforced last year's winners.

Indices Stressed by the Two Economies

Growth and value indices typically split the parent index into two halves of approximately equal market value. Defining the styles was always hard, since some stocks have both characteristics and some have neither, but future-growth stocks have grown too large to all fit in the Growth indices. For example, memory producer Micron contributed enormously to many Value indices.

Emerging markets tell the same story with countries instead of styles. Taiwan and Korea drove roughly three quarters of emerging market returns over the past year, mostly from three semiconductor makers. TSMC alone is 14% of the index, the three approach a quarter of it, and their combined profits are on track to exceed Apple, Amazon, and Alphabet together. Even real estate is affected, with data centers now among the largest constituents of REIT indices.

Investors seeking today's economy through value, emerging markets, or real estate hold substantial exposure to AI and the future economy.

The Conservative Investor's Dilemma, Continued

It was a difficult quarter for low-risk investors. Discipline is usually tested by holding through a decline; this quarter tested it by sitting out a melt-up. An investor who holds through volatility feels prudent; one trailing a euphoric market feels left out, though both are doing the same correct thing.

Pre-Covid, inflation was too low, shocks were deflationary, and bonds were free insurance since monetary policy fights recession and deflation simultaneously. Post-Covid, the shocks are inflationary, and inflation that hurts the economy hurts the hedge.

We warned at year-end that traditional defensive assets had become less reliable. Gold then lost value during a military crisis in the first quarter and had its worst quarter since 2013 in the second. However, this coincides with a reversal of speculative interest, which allows gold to return to its previous risk characteristics.

A conservative portfolio must spread risk across many imperfect hedges, sized by what they can bear. Intermediate Treasurys remain useful, providing enough yield and duration to cushion an equity decline without the long end's exposure to deficit-driven supply. TIPS, minimum volatility equities, real assets, and international diversification each carry a necessary share of the defense.

Source: Bloomberg

Owning Both Economies

Leading AI firms are handing essentially all free cash flow to infrastructure that costs roughly twice what it should, as competition for power, land, and chips lets suppliers charge scarcity prices. We know houses built when construction costs are high will fall when costs normalize. Markets are rewarding unusually inefficient investment. There is no guarantee of winner-take-all; a latecomer buying capacity at normal prices could surpass early participants who overpaid. The productivity gains and market value of AI may go to the companies that use it rather than the few that spent fortunes pioneering it.

Exposure to the future economy also need not be a single bet on U.S. technology. Chinese AI firms offer a partially independent claim on the same future; this year China's megacap technology companies performed poorly while domestic A-shares did well, nearly the opposite of the U.S.

Europe is the clearest exposure to today's economy. Left out of the AI boom, it remains a rich and diverse economic zone. Its heavy weighting in banks, energy, and industrials provides diversification for a portfolio concentrated in the future economy.

European exposure can also be obtained through corporate credit. This is economically justified as European companies have a relatively higher reliance on debt rather than equity compared to U.S. companies. And Europe may have its AI comeback on better terms: data centers built after the surge at normal prices, with AI productivity offsetting the short work week.

AI is effectively a systematic risk factor: it pervades many asset classes, carries both risk and return, and has no hedge other than avoiding it. Risk models with short-term statistical factors are already detecting it, named or not.

Private Markets Catch Up

Private markets are catching up by becoming ordinary. After some scares and major redemptions, private debt is settling down; investors should not expect extraordinary returns as yields normalize toward risk-adjusted public credit. Private equity remains quietly present, with abundant committed capital competing for deals and moderating returns.

One factor differentiating private equity: AI startups are forming quickly, and almost entirely outside public markets. They are capital-light, so public listing is inefficient for them, and private equity's capital surplus makes funding easy.

In both, funds and technology keep improving, lowering fees and easing illiquidity. This supports our longstanding thesis that private markets are slowly turning into another asset class, helpful but not exceptional. Investors can meet their goals without them, but could enhance performance by using them optimally.

Look Ahead: Midyear Scorecard

At the start of the year we made four probabilistic predictions: inflation would rise a bit; the economy would slow without recession; signs of capital misallocation in AI would emerge late in the year; and global markets would rise. At the half: inflation rose, though the war did more of the work than the tariff pass-through we named; the economy slowed a bit; the misallocation arguably exhibited as volatility over the scale of infrastructure spending and a reallocation from AI software to hardware; and markets rose narrowly. Not bad, but not entirely for the reasons given. Playing probabilities means probably being right for imperfect reasons and wrong for good ones.

For the second half, we state what structure already implies rather than predict:

- Stocks should rise over time because investors price them with a risk premium; high valuations shrink that premium but do not eliminate it.

- Bonds have reasonable coupons in real terms.

- Tariffs should have minimal market impact now that markets understand trade policy.

- Inflation will fall more slowly than it rose and long rates will not fall much despite policy pressure.

- Concentration will eventually resolve: either the future economy grows into its prices, or prices come back to economic reality. The diversified investor will survive both scenarios.

Most worries can be sorted. The real question is whether AI proves an asset bubble or an economic disruptor, and diversification is the only useful response while it stays open. Worries to set aside: Fed meddling (Warsh is taking the job seriously), Iran headlines, and month-to-month inflation prints. AI valuations will keep downplaying current events until a major counterexample arrives.

We do not know the future for the middle east, the Fed, or AI – no one does, and prices already reflect that. But we can hold portfolios that do not require any of these questions to resolve favorably.

Conclusion

Both economies are real. The future economy will arrive in some form, though probably not the form currently priced, and today's economy will adapt and hold value within it. The deep question is how much to hold of each: just as investors ask whether to take more or less risk than average, they should ask whether to hold more or less of the future economy than the market already does. The answer depends partly on horizon: the longer the horizon, the more of the future an investor will live in, and the more of it their portfolio can afford to own.

The second quarter rewarded speculation and tested caution. In such times, envy strains discipline as much as a fear does in a downturn. We see record trading producing record bank profits, paid by investors who lose more often than they gain from short-term activity.

We remain long-term optimists across scenarios. Markets work well with technological advances, which supports long term investors. AI, even at current capability levels, is among the most important technological revolution of our lives, and the world is generally moving forward. Our answer is unchanged: be conscious of risk, let the market do the work of pricing the unknown, and diversify deliberately across both economies.