A Primer on Risk and Long-Term Investing

When selecting investments, one might be tempted to select funds claiming better expected returns. The thought process is that higher average returns over time will result in greater wealth at the end of the investment period.

However, there is something missing from this quick analysis that can kill investment performance over time: consideration of risk. Risk must be managed over time for good investment performance, because in spite of a great looking average return, large negative returns from risky investments have an outsized impact on performance and can quickly wipe out gains accumulated over time.

The key to understanding this core concept of investing is that returns compound multiplicatively. Over each period, final wealth is calculated by multiplying one hundred percent plus the return times the initial wealth. Consider a fund where two successive returns cancel each other out, so that after two periods the investor’s wealth hasn’t changed. To undo a first period return of, say, +10%, the second period’s return only needs to be -9.09%, since (100% + 10%) * (100% - 9.09%) = 100%, whereas to undo a negative return of -10%, the positive return must be +11.11%. Larger positive returns are needed to balance negative returns. For larger size returns the effect is even more dramatic: a +50% return is undone by a -33.33% return, whereas a -50% return requires a +100% return to offset it. Greater positive and negative returns correspond to higher risk and higher average (arithmetic mean) returns, for funds with equal performance through the same period. For high-return risky funds, occasional large negative returns are performance killers. Table 1 shows the positive returns needed to restore wealth after a negative return, and the average return associated with the 2-period history. Negative returns need even greater positive returns to break even, and the larger the negative return, the greater the positive return must be in proportion. Greater risk increases the likelihood of large negative returns, even though it may be associated with greater average return. A devastating negative return can take years to recover from since larger returns occur far less frequently than smaller ones.

|

Negative Return |

Positive Return Needed to Restore Wealth |

Average Fund Return |

|

-1% |

1.01% |

0.0% |

|

-2% |

2.04% |

0.0% |

|

-5% |

5.26% |

0.1% |

|

-10% |

11.11% |

0.6% |

|

-15% |

17.65% |

1.3% |

|

-20% |

25.00% |

2.5% |

|

-25% |

33.33% |

4.2% |

|

-30% |

42.86% |

6.4% |

|

-35% |

53.85% |

9.4% |

|

-40% |

66.67% |

13.3% |

|

-45% |

81.82% |

18.4% |

|

-50% |

100.00% |

25.0% |

Table 1: Positive returns (right column) needed to compensate for negative returns (left column).

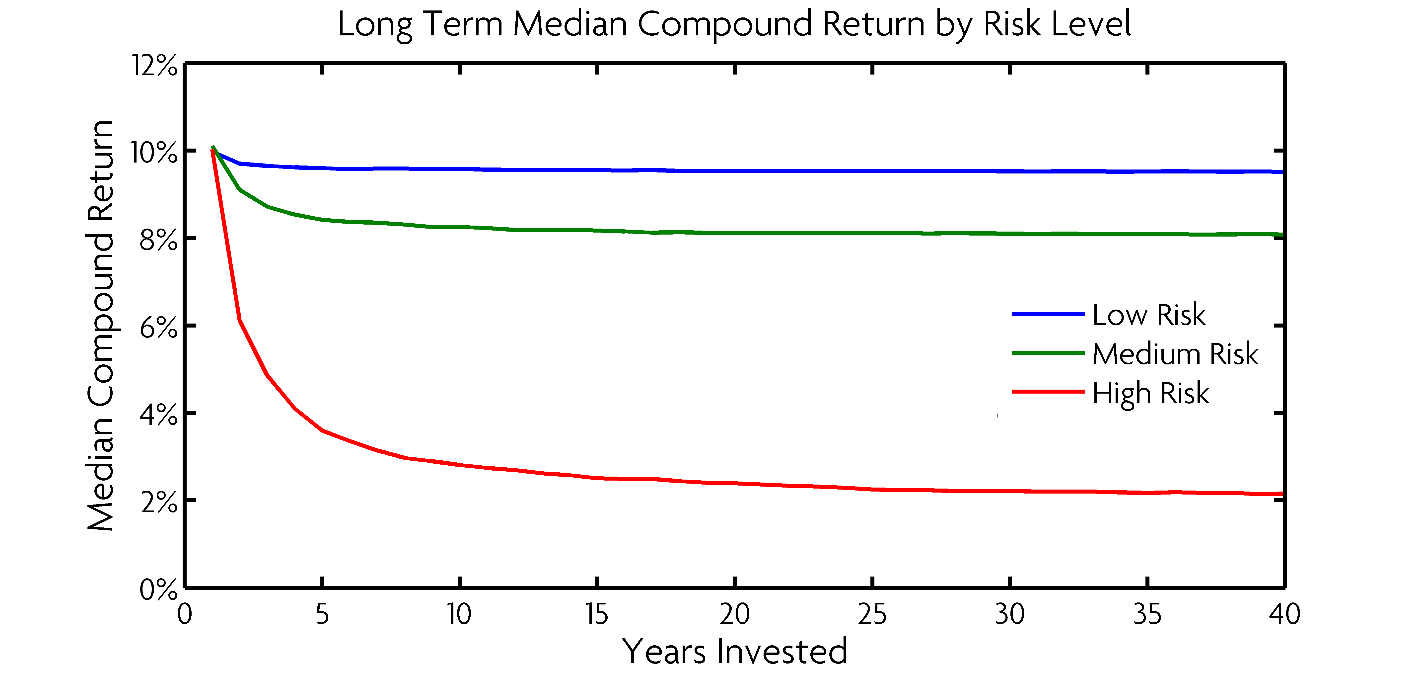

Consider the following Monte Carlo simulation experiment: we have three funds to choose from, all with 10% annual expected return. Their risks are low (10%), medium (20%), and high (40%), as measured by annualized standard deviation. Over time, the riskier funds tend to exhibit more negative single-period returns, with this tendency becoming certainty as the investment period becomes longer. In a simulation of 1,000,000 possible histories, the median realized annual returns are shown in Figure 1.

Figure 1: Long term median performance of three funds, all with nominal 10% expected return. Medians were selected from 1,000,000 Monte Carlo simulations.

As can be seen, a high risk fund with a nominal 10% return gets only 2% realized return when the risk is high. The low risk fund in the example may have unrealistically low risk for a high (10%) annual return, which means that in practice, funds with high expected returns cannot be expected to deliver that over a long term investment. Moreover, these estimates are optimistic since fees and other costs have not been factored in, and also because that 10% figure would be an estimate and is unlikely to be the real expected return for real investments.

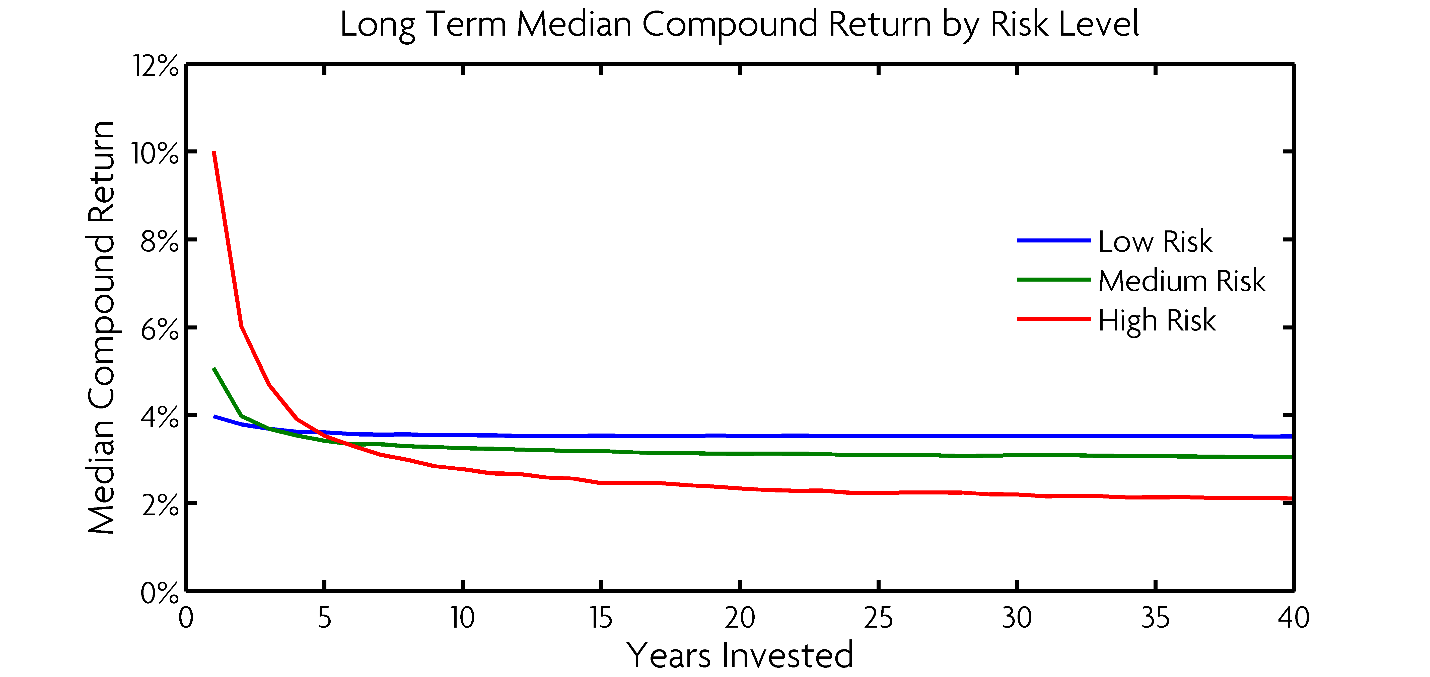

Considering that risk may be better estimated than return, and that differences in predicted return may not be large among candidate investments, risk might be the most important deciding factor for selecting long term investments. Consider our example again, but with the lower risk funds having lower returns than the higher risk ones. This may be a more realistic example in terms of consumer choice. The results for returns of 4%, 5%, and 10%, with annualized standard deviations of 10% (low), 20% (medium), and 40% (high) are shown in Figure 2.

Figure 2: Long term median performance of three funds, with nominal 4%, 5%, and 10% returns, and 10%, 20%, and 40% standard deviations. Medians were selected from 1,000,000 Monte Carlo simulations.

The losses due to risk over the longer periods outweigh the differences in expected return. The final values of the three funds end up upside down from their nominal annual return rates. The best performing fund here is the least attractive when considering only expected return.

Although these Monte Carlo examples are purely hypothetical, they effectively illustrate a very real concept which greatly impacts real long-term investment performance. There is indeed an observable and surprisingly substantial penalty for high-risk investing over the long term which undermines performance and negates the purported higher returns of risky investments. Negative returns have a far more lasting and devastating effect on portfolio value than equally sized positive returns.

Of course, there are some high risk and return funds that are worthy investments. In such cases, they can be managed within a portfolio through appropriate diversification and quantitative risk management such as optimization. Much of the high risk can be diversified away by balancing with exposure to other low risk or even negative correlation funds. The danger here is having unmanaged exposure to high risk funds without any balanced exposure to other funds to mitigate this risk.

It may be tempting to jump at high-return funds for the promise of the possibility of gaining more wealth, but the overwhelming likelihood over the long term is that more potential wealth will be lost due to the high risks of high-returning investments. It is far more sensible to invest in well-diversified risk-managed funds whose nominal returns may appear less attractive. Proper risk management is ultimately connected to better performance and may be more important for selecting funds than seeking high returns.

comments powered by Disqus

Need more information?

Contact us to find out how we can work with you.