Q3 2021 Market Perspectives: "A Global Shift"

After beginning the quarter on a relatively upbeat note, familiar themes returned as fears of inflation, ambiguity over the end of the pandemic, and uncertainty about the future of Chinese capitalism raised concerns for investors. Markets vacillated between these concerns and cautious optimism for economic growth emerging from the pandemic. As a result, many markets ended the quarter close to where they started.

Market Performance

This was a challenging quarter for both stock and bond investing. Negative or flat returns were seen from nearly all major asset classes. Equities are still strong year-to-date as stock markets hit record highs more than 50 times this year before losing momentum in early September. The S&P 500 is up 15.9% for the year and was up as much as 6% this quarter before ending with a meager gain of 0.6%. This quarter, small cap stocks declined by 4.4% and international equities underperformed U.S. markets by over 3% with Asia-Pacific markets up 1.6% and China pulling emerging markets down 7.4%. U.S. fixed income returns were flat, with core U.S. aggregate bonds up 5 basis points after a sharp decline in late September offset the quarter’s prior gains.

Strategy Performance

In Q3, New Frontier Multi-Asset Income ETF portfolios outperformed the benchmarks, supported by a relatively overweight allocation to U.S. dividends that outperformed international dividends, along with positive returns added by U.S. REITs and global infrastructure stocks.

New Frontier Global Core and Tax-Sensitive ETF portfolios slightly underperformed the stated benchmarks, primarily due to the underperformance of small-cap and emerging market equities. Fixed income returns were mixed but largely muted. Conservative and balanced portfolios did better than aggressive portfolios on both an absolute and relative basis, helped by less exposure to riskier equities while overweighting U.S. minimum volatility stocks and Asia-Pacific market equities. Gains from large cap growth stocks were canceled out by losses from risky equities for aggressive portfolios.

Performance Contribution

Long Treasurys ended the quarter slightly positive, but had been the best performing bond for the majority of the quarter until the Fed signaled tapering was likely in November and the 10-year yield climbed back up. TIPS took the lead as inflation concerns remained. The dollar rose to a one-year high, boosted by increased expectations for a reduction in Fed liquidity support and concerns over global growth slowdown. A stronger dollar weighed on returns of international treasuries and emerging markets debt, both of which ended in negative territory.

A rising yield in late September put downward pressure on equity valuations, especially for richly-valued growth stocks, but over the quarter U.S. large cap growth stocks remained the largest contributor to portfolio performance. At the other end of the spectrum, China was the biggest detractor from the performance for the quarter and also for the year, due to a broad-based regulatory crackdown from tech to entertainment, and growing concerns over Evergrande and a potentially broader real estate and debt crisis.

Market Insights

The potential for government gridlock, shutdowns, or potential bond default is never positive, but heightened divisions between political parties are having a particularly noticeable effect on markets. In the previous default scare, some investors were initially puzzled to see increased demand for Treasurys – the very asset that could default – but the market quickly figured out the reality that the damage to other assets could be far greater. This experience is now factored into market expectations, and surprises are less likely to be repeated.

Bonds have been interesting. High yield, generally considered the riskiest of bonds, has had lower volatility than corporate or Treasury bonds this year. Rates have been up and down (and part way back up again), but corporate spreads have been a dampener. Additionally, inflation, transitory or otherwise, has pushed real rates further into negative territory.

Is The U.S. Market Exceptional?

U.S. markets have once again outperformed international equities. For nearly a century, U.S. investors have been in the enviable and unique position of having a rational home bias for the largest and most consistently rewarding equity market in the world. In the absence of information, assigning equal weight to every major market or region could be sensible, but we allocate very roughly half of equity investments to U.S. asset classes. We do so deliberately with the understanding of the risk and return tradeoff—the U.S. market must still obey the laws of economics and cannot provide long term returns without growth, but thanks to open transparency and responsibility to shareholders, it remains exceptional in its ability to reward investors for achieved economic growth.

Relative Interest Rates and Currency Returns

The dollar rose with interest rates in the U.S. this quarter. To understand this relationship, note that U.S. yields are significantly higher than any other major market. The U.S. is also broadly perceived as the most credit worthy and least risky bond issuer. Therefore, from the perspective of an international investor, U.S. Treasurys are particularly attractive investments. Market forces do not generally allow superior investments to remain available forever, so the U.S. will likely not remain the highest returning treasury market for international investors. Ultimately, the dollar should weaken or U.S. rates will converge with others either by falling to their low levels or with international rates rising.

Trends

The retail investing trend seen throughout the year continued this quarter. Although Gamestop and Reddit made fewer headlines this quarter than earlier in the year, Bitcoin and collectibles markets with sales of $200,000 Pokemon cards and $60 million NFTs, continuing to provide further evidence of retail demand for investments. Retail investing has the potential to disrupt the institutionally priced U.S. equity markets and influence asset prices at least in the near term.

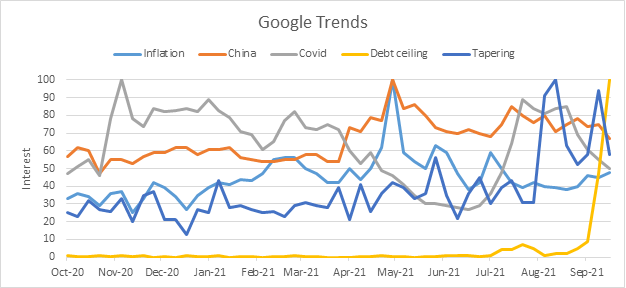

Source: Google

On a broader level, Google trends show inflation, China and the pandemic continue to be present concerns with emerging expectations of tapering. Prediction markets expect extreme political brinkmanship, and support a real possibility of the U.S. defaulting on its debt for the first time in history.

The Economy

While the pandemic recovery has continued with regard to higher economic growth and employment, there have also been mixed economic signals. Employment forecasts by economists have continued to be unreliable as businesses and consumers continue to adjust their reactions to the virus as new information becomes available.

Markets have largely shrugged off the narrowly averted government shutdown, but the remote devastating possibility of a government default remains. As of 9/30/2021, PredictIt markets put the odds of the debt ceiling being resolved by the presumptive deadline of October 15 at only 48%. This contract likely overstates the chance of a full default, as other emergency measures can buy time, but self-inflicted damage to credibility at a time when there are broad concerns about asset valuations could start a crisis of investor confidence. In this context, a comedically inspired trillion-dollar coin seems less absurd, although far from desirable.

On a more rational note, some degree of economic stimulus has been priced into the market since Democrats took control of the Senate in January. However, much uncertainty remains over the scope of the stimulus. Markets will react as this becomes resolved, but shifts in economic policy can have a greater and more immediate impact on the economy than a fiscal stimulus.

Meanwhile, fiscal stimulus is finally tapering. Chairman Powell deserves recognition for leading the Fed across two disparate administrations. Powell and the Fed understand two important lessons of the past—the value of clear communication, and a sophisticated modern understanding of inflation in the economy. This has been demonstrated by his masterfully clear communication of the much-anticipated taper. As a result, the market took the final news—that tapering is likely starting in November and ending next summer—in stride. This is a stark contrast to the 2013 comments from Bernanke leading to the “taper tantrum.”

Interest rate risk remains high, but in the U.S., the 10-Year Treasury yield rose slightly from 1.45% to 1.52% over the quarter. Rates around the world generally followed the pattern of the U.S. market and declined for most of the quarter before rising precipitously in the final weeks to end close to where they began.

China

China completed its retransformation back to an emerging market after briefly leading the developed world in the early pandemic. Financial, economic, and political factors contributed, with investors concerned about the debt capacity of the Chinese economy. Much of the retail, municipal, and local debts are kept deliberately difficult to quantify by the ruling party, but the high-profile demise of the Evergrande real estate firm is seen by some as an indication of the decline of Chinese real estate market that has been anticipated for over a decade. Evergrande may be both the tip of the iceberg – as there’s more debt out there than we know – and the tipping point for a spiraling crisis of real estate losses and default.

Energy shortages are hindering manufacturing, and neither the trade war with the U.S., nor global supply chain issues relented. The biggest concerns were of political uncertainty as President Xi’s regulatory restrictions went into effect, including the ban on both the mining and transacting of Bitcoin, where China was once leading the world in energy intensive Bitcoin mining.

Foreign investors faced many headwinds in China, calling market valuations into question. Chinese markets suffered from economic and political uncertainty over the new regulations. Recent market returns in China remind investors of the disconnect between economic growth and market returns. Though market returns from 2010 through 2020 were reasonable, investors should remember that the first investible MSCI China index was flat from 1990 to 2010 as China’s GDP soared.

Inflation and Asset Prices

Commodities have minimal direct impact on our portfolios, but they have the potential to be the driving force of non-transitory inflation. Oil and natural gas prices have risen 3% and a spectacular 62% for the quarter, and 56% and 132% for the year. Unlike so much of the global economy bolstered by government support or dependent on softer measures of productivity, commodity supply is an objective measure that cannot be explained away with positive narratives about the work from home economy. These prices are an uncomfortable reminder that pandemic productivity and bottlenecks have serious economic consequences.

Conclusions and a Look Ahead

Low rates, high equity valuations, and no clear end in sight for the pandemic or U.S. or Chinese politics should prompt investors to maintain a risk target they are comfortable with rather than speculate on fixed income, equities, or a highly volatile retail fad.

DISCLOSURES: Past performance does not guarantee future results. As market conditions fluctuate, the investment return and principal value of any investment will change. Diversification may not protect against market risk. There are risks involved with investing, including possible loss of principal.